California May Have a New Homebuyer Assistance Program in 2026

California homebuyers may have a major new assistance program to watch in 2026.

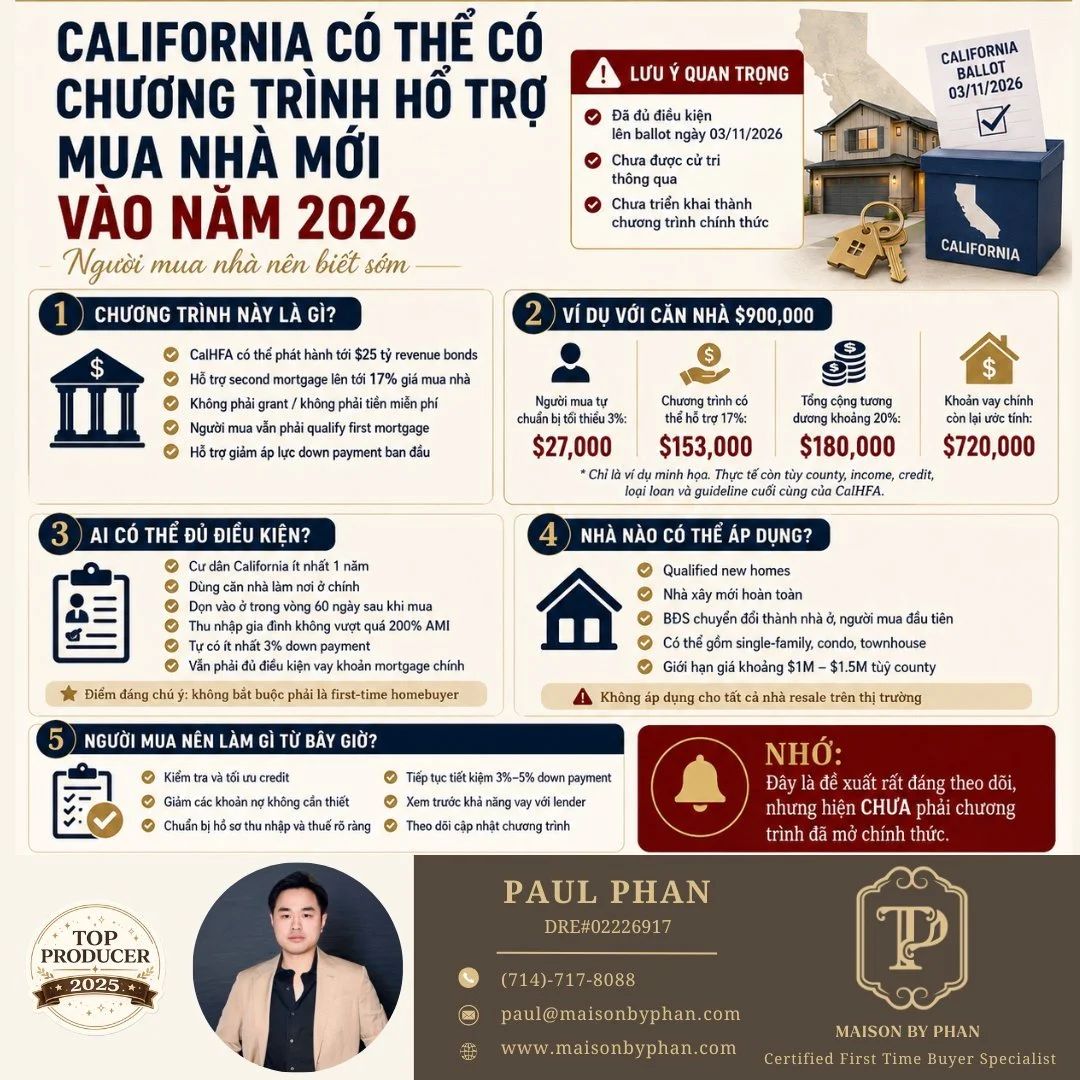

On April 21, 2026, the California Secretary of State announced that a proposed initiative titled “Creates Loan Program for Middle-Income Buyers of Qualified New Homes” became eligible for the November 3, 2026 General Election ballot. This proposal is designed to help middle-income buyers purchase qualified new homes through a second mortgage program administered by CalHFA.

It is important to understand one key point first:

This proposal has qualified for the November 2026 ballot, but it has not yet been approved by voters and is not currently an active assistance program.

Still, for buyers planning to purchase a home in California within the next one to two years, this is worth following closely. If approved, early preparation could make a significant difference.

What Is This Proposed Program?

If approved by voters, the measure would authorize up to $25 billion in bonds to provide eligible buyers with fixed-rate mortgage assistance for up to 17% of the purchase price of a qualified new home. The program would be administered by the California Housing Finance Agency, also known as CalHFA.

This is not described as a free grant. It would be a second mortgage, also referred to in the Legislative Analyst’s Office analysis as a “middle-class homeownership loan.”

That means buyers would still need to qualify for their main mortgage, meet lender guidelines, show income, meet credit requirements, and have an acceptable debt-to-income ratio.

The purpose of the proposal is to reduce the initial down payment burden for qualified middle-income buyers, especially those who may have stable income but struggle to save a large down payment in California’s high-cost housing market.

Example: A $900,000 Home

Here is a simple example of how the proposal could work if it becomes law and the buyer qualifies.

For a $900,000 qualified new home:

ItemExample AmountBuyer’s minimum 3% down payment$27,000Potential program assistance up to 17%$153,000Combined amount toward purchase$180,000Estimated remaining first mortgage$720,000

Instead of having to prepare the full 20% down payment amount on their own, a qualified buyer may be able to contribute 3% while the program provides additional second mortgage support.

This is only an example. The actual numbers would depend on final program rules, county limits, home price, income, credit, loan type, interest rate, debt-to-income ratio, and CalHFA guidelines if the measure is approved.

Who May Qualify?

Based on the official summary and Legislative Analyst’s Office analysis, the proposed eligibility requirements include several important conditions. Buyers would generally need to:

RequirementWhat It MeansCalifornia residencyBuyer must be a California resident for at least one yearPrimary residenceBuyer must plan to live in the homeIncome limitHousehold income must be below 200% of the area median incomeBuyer contributionBuyer must pay at least 3% downMain mortgage qualificationBuyer must still qualify for the primary mortgageOccupancy timingBuyer is expected to occupy the home as a primary residence after closing

One especially important detail is that this proposal is aimed at middle-income buyers. It is intended for people who may be able to afford a monthly mortgage payment but have difficulty saving enough for the initial down payment.

Another notable point is that the official summary does not describe the proposal as being limited only to first-time homebuyers. However, buyers should wait for final CalHFA rules if the measure passes before relying on any specific eligibility interpretation.

What Types of Homes May Apply?

This proposal would not apply to every home on the market.

According to the official summary, the assistance would apply to a “qualified new home,” which generally means:

Eligible Property TypeDescriptionNew constructionA newly built homeConverted residential propertyA first sale of a property converted from nonresidential useProperty typesMay include single-family homes, condos, townhomes, or similar qualified propertiesPrice limitsExpected to be below approximately $1 million to $1.5 million, depending on the county and adjusted annually

This means buyers should not assume that any resale home would qualify. The current proposal is focused on qualified new homes and certain converted properties.

Why Buyers Should Pay Attention Now

Even though this is not an active program yet, buyers who are planning for 2026 or 2027 should start preparing early.

Large homebuyer assistance programs can attract strong demand. If this proposal is approved and later implemented, buyers with organized documents, stronger credit, clean income records, and lender readiness may have an advantage.

Buying a home is not only about finding the right property. It is also about being financially prepared at the right time.

What Buyers Should Do From Now

Buyers who may want to take advantage of future assistance programs should start with the basics:

StepWhy It MattersCheck and improve creditBetter credit may help with loan approval and pricingReduce unnecessary debtLower debt can improve debt-to-income ratioFile taxes clearly and accuratelyLenders need consistent income documentationSave at least 3% to 5% downEven assistance programs usually require buyer contributionSpeak with a lender earlyHelps buyers understand realistic purchase powerResearch new construction optionsThis proposal is focused on qualified new homesFollow official updatesFinal rules will matter if the measure is approved

Preparation now can give buyers more flexibility later.

Important Reminder

This proposal is worth following, but it is not yet a final program.

It has qualified for the November 2026 ballot, but California voters still need to approve it. If approved, CalHFA would still need to issue final guidelines, program requirements, lender procedures, and implementation details.

For now, buyers should treat this as a potential opportunity, not a guaranteed benefit.

Final Thoughts

California’s housing market remains challenging, especially for middle-income families who have stable income but struggle with the large upfront cost of buying a home.

This proposed 2026 program could become an important tool if voters approve it. However, the best strategy for buyers is not to wait until the last minute. Start preparing credit, income documents, savings, and lender conversations now.

The buyers who are ready early are often the buyers who are in the best position when the right opportunity appears.

If you are planning to buy a home in California in 2026 or 2027 and want help preparing your homebuying strategy, Paul Phan can help you understand your options, connect with lending resources, and create a plan that fits your budget and goals.

Contact

Phat Phan (Paul Phan)

Maison by Phan | Frontier Realty

DRE#: 02226917

Call/Text: 714-717-8088

Email: Paul@maisonbyphan.com