When Refinancing Makes Sense — and When It Can Cost You More

Refinancing often sounds simple. You replace your current mortgage with a new loan that offers a lower interest rate or different terms. On the surface, that can seem like an easy way to reduce your monthly payment and save money.

But refinancing is not something homeowners should do just because they hear rates have come down.

In some situations, refinancing can be a smart financial move that saves a household a substantial amount of money over time. In other cases, it may lower the monthly payment slightly while actually increasing the total cost of the loan over the long run. That is especially true when a refinance resets the loan term, adds new fees, or extends the amount of time interest is being paid.

The key is understanding that refinancing is not automatically good or bad. It depends entirely on the numbers, the timing, and the homeowner’s long-term plan.

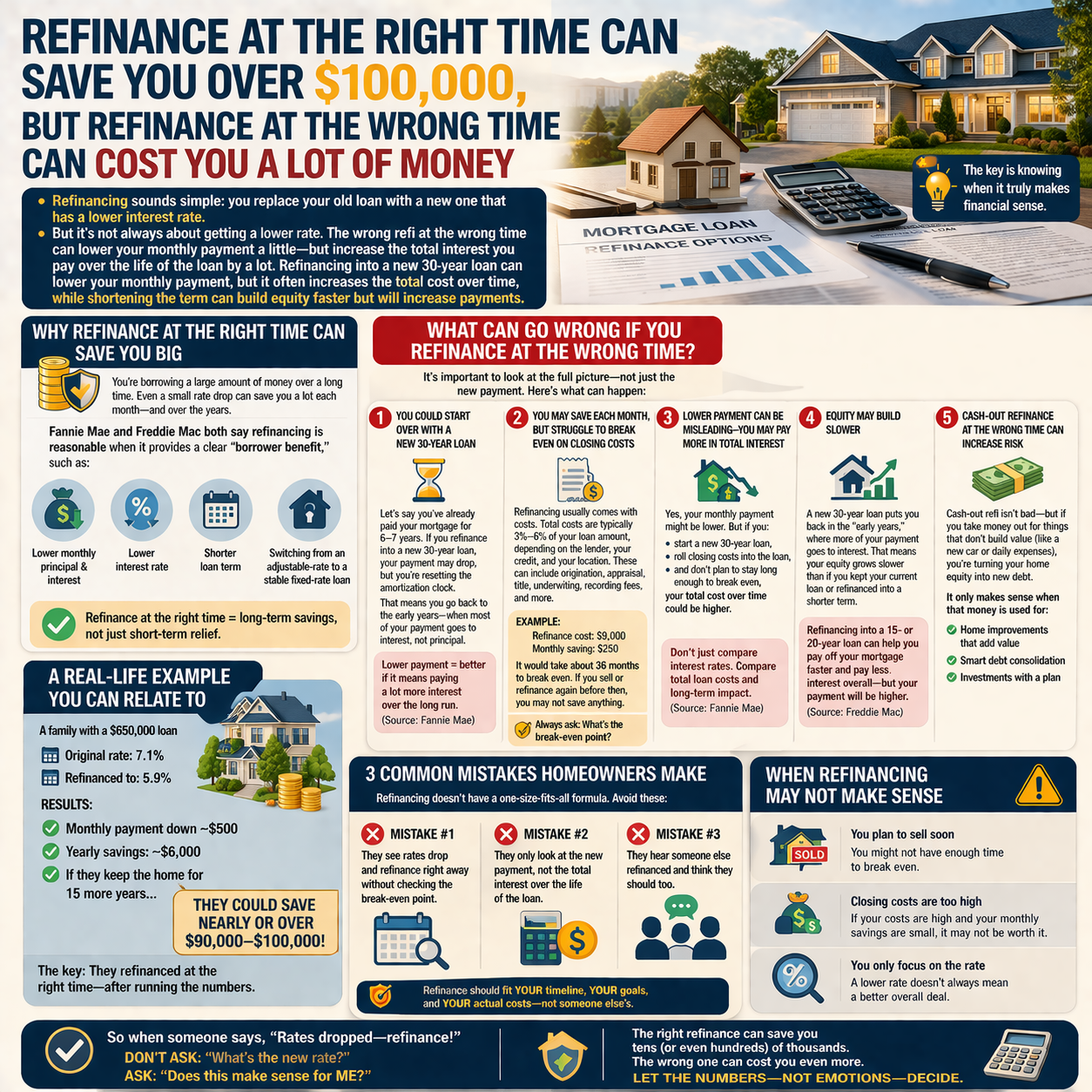

Why Refinancing at the Right Time Can Save So Much Money

Mortgage loans involve large balances over long periods of time. Because of that, even a modest reduction in interest rate can create meaningful savings when spread across many years.

If a homeowner refinances from a higher rate into a meaningfully lower one, the monthly principal and interest payment may decrease. In the right situation, refinancing can also help remove mortgage insurance, shorten the loan term, or convert an adjustable-rate mortgage into a more stable fixed-rate product. When that happens, the benefit is not just emotional relief from a lower payment. It can be a real long-term financial improvement.

That is what a good refinance should do. It should create a clear borrower benefit, not just look attractive at first glance.

The Biggest Mistake: Looking Only at the New Monthly Payment

One of the most common mistakes homeowners make is focusing only on the new monthly payment.

A lender may present a refinance option that lowers the payment by a few hundred dollars, and at first that sounds like an obvious win. But if that lower payment comes from starting over with a brand-new 30-year mortgage, the homeowner may end up paying interest for much longer than expected.

A lower payment does not always mean a better deal.

If you have already been paying your mortgage for six or seven years, your existing loan has already moved beyond the very earliest stage of amortization. When you refinance into a new 30-year loan, you are restarting that clock. That means a large share of the payment may once again go toward interest rather than principal. The payment may feel lighter month to month, but the total interest paid over time may rise significantly.

How Refinancing Can Quietly Increase Long-Term Costs

This is where many homeowners get caught off guard.

A refinance may reduce the monthly payment while also increasing the total borrowing cost because of three factors happening at once. First, the homeowner may be resetting into a longer term. Second, the refinance usually comes with closing costs. Third, those costs may be rolled into the new loan balance rather than paid separately.

When that happens, the homeowner may feel immediate relief but unknowingly commit to a more expensive long-term structure. The loan looks better today, but the lifetime cost may be worse.

That is why refinancing should never be evaluated only by rate or payment. It has to be evaluated by the total financial picture.

Why Break-Even Point Matters So Much

Every refinance has a cost.

There may be lender fees, appraisal fees, title charges, underwriting fees, recording fees, and other transaction costs. Depending on the loan and lender, those costs can be substantial.

That is why one of the most important questions to ask is not just, “How much will I save each month?” but also, “How long will it take me to recover the cost of this refinance?”

For example, if refinancing costs $9,000 and the new mortgage saves $250 per month, the break-even point is about 36 months. If the homeowner plans to sell the property or refinance again before that point, the refinance may never actually produce meaningful savings. In that case, the transaction may not be worth doing at all.

Refinancing Can Also Slow Down Equity Growth

Another issue many homeowners overlook is how refinancing can affect equity growth.

When a loan resets to a fresh 30-year amortization schedule, more of each monthly payment usually goes toward interest at the beginning of the new loan. That means equity may build more slowly than it would have if the homeowner stayed with the current mortgage or refinanced into a shorter term.

For homeowners whose goal is to pay down the home faster, a shorter refinance term such as 15 or 20 years may make more sense. While that often increases the monthly payment, it may also help reduce total interest and build equity more quickly. The right choice depends on whether the homeowner’s priority is payment relief, long-term savings, or faster payoff.

When Cash-Out Refinancing Becomes Risky

Cash-out refinancing is another area where homeowners need to be careful.

A cash-out refinance is not automatically a bad idea. In some cases, it can be a useful tool for value-adding improvements, smart debt restructuring, or planned investment. But when homeowners use it casually for spending, consumer purchases, or costs that do not improve their financial position, they may be turning home equity into new long-term debt.

That can weaken their overall financial footing.

Home equity is one of the most important assets many homeowners have. Using it without a clear purpose can increase financial risk rather than improve financial flexibility.

A Real-Life Example of Why Timing Matters

Consider a household with a mortgage balance of around $650,000. If their original rate was 7.1% and they refinanced into a new loan at 5.9%, the monthly savings could be around $500. That translates to roughly $6,000 per year. If they keep the property for another 15 years, the total savings may approach or even exceed $90,000 to $100,000.

That is the power of refinancing at the right time.

But what made that refinance worthwhile was not just the lower rate. It was the fact that the numbers were reviewed carefully, the savings were real, and the homeowner planned to keep the property long enough to benefit from the change.

Three Common Ways Homeowners Refinance at the Wrong Time

There are a few patterns that come up again and again.

The first is refinancing just because rates dropped without calculating the break-even point.

The second is looking only at the new payment instead of the total interest cost over time.

The third is refinancing simply because someone else did it, without checking whether it actually makes sense for that specific household.

Refinancing is not a one-size-fits-all decision. What works well for one homeowner may be a poor decision for another. The right answer depends on how long the home will be kept, what the financial goals are, and what the full cost of the new loan really looks like.

When Refinancing Usually Does Not Make Sense

There are several situations where refinancing may not be worth it.

If a homeowner plans to sell soon, there may not be enough time to recover the refinance costs.

If the lender fees and closing costs are high, even a lower payment may not justify the transaction.

If the refinance looks attractive only because of the rate, but the total costs and long-term interest are worse, it may not be a true savings opportunity.

And if the homeowner is resetting into a new 30-year term after already making years of payments, the lower monthly number may hide a much more expensive total outcome.

When Refinancing Is Worth Considering

Refinancing is usually worth considering when there is a clear financial goal.

That may include lowering the rate enough to create meaningful real savings, removing PMI once enough equity has been built, converting an adjustable loan into a fixed-rate mortgage for more stability, shortening the term to pay off the home faster, or restructuring monthly cash flow based on a major life change.

The best refinance is not simply the one with the lowest advertised rate. It is the one that actually improves the homeowner’s situation in a measurable way.

Final Thoughts

Refinancing can be a powerful financial tool, but only when it is used strategically.

Done at the right time, it may save a homeowner tens of thousands of dollars, improve monthly cash flow, or create more stability for the future. Done at the wrong time, it may add unnecessary costs, reset the loan in an unfavorable way, and reduce the long-term benefit of homeownership.

That is why the first question should never be, “What is the new rate?” The better question is, “Does refinancing actually make sense for my situation?”

A smart refinance decision is not based on headlines or what other people are doing. It is based on numbers, goals, timing, and the full long-term impact of the new loan.

If rates dropped tomorrow, would you know whether refinancing would actually help your situation, or would you want to run the numbers first?

Contact

Phat Phan (Paul Phan)

Maison by Phan | Frontier Realty

DRE#: 02226917

Call/Text: 714-717-8088

Email: Paul@maisonbyphan.com